Kasper Johansson

I’m a Quantitative Researcher at Citadel’s Global Quantitative Strategies team in New York. Previously, I completed my PhD in Professor Stephen Boyd’s group at Stanford, where my research focused on convex optimization applied to quantitative finance. Before Stanford, I was a research fellow at Harvard and a research intern at Caltech. I hold a BSc in Physics and an MSc in Machine Learning, both from KTH Royal Institute of Technology in Stockholm, Sweden.

news

| Jun 6, 2025 | My dissertation thesis has been published: Convex Optimization in Quantitative Finance. |

|---|---|

| Mar 29, 2025 | We published a preprint of our manuscript A Tax-Efficient Model Predictive Control Policy for Retirement Funding. |

| Jan 24, 2025 | I gave a talk on Markowitz Portfolio Construction Using CVXPY at BlackRock’s portfolio construction summit. |

| Dec 11, 2024 | I defended my PhD thesis: Convex Optimization in Quantitative Finance. |

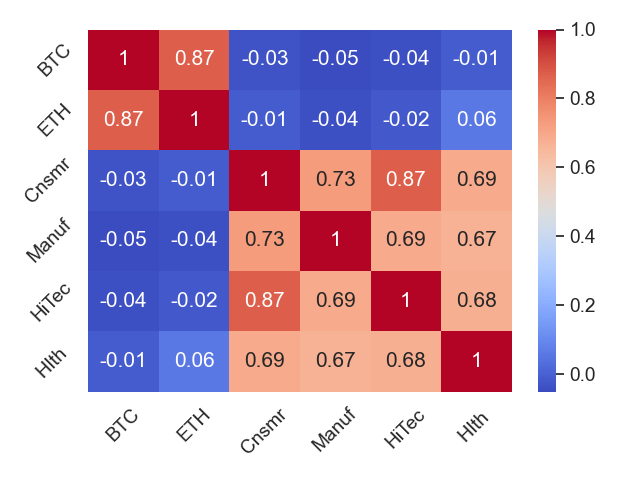

| Nov 16, 2024 | We published a preprint of our manuscript Simple and Effective Portfolio Construction with Crypto Assets. (Now published in Crypto Insights and Trends, Competition Policy International, 2025.) |

| Jun 11, 2024 | We published slides illustrating several uses of Convex Optimization in Quantitative Finance . |

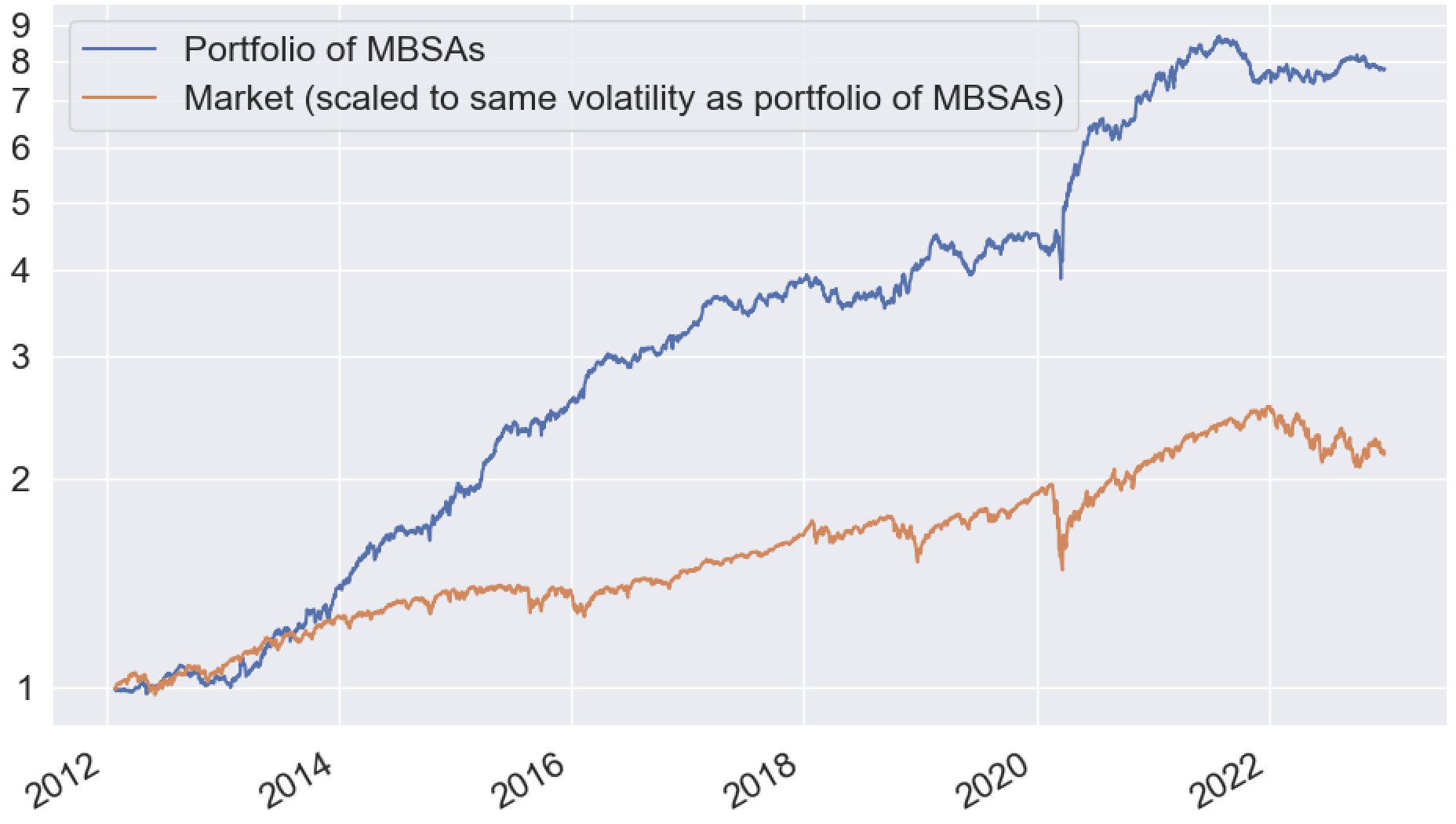

| Jun 8, 2024 | We published a preprint of our manuscript A Markowitz Approach to Managing a Dynamic Basket of Moving-Band Statistical Arbitrages . |

| Mar 21, 2024 | I presented our work on covariance prediction in finance at the Fidelity Investments seminar series. The slides are available here. |

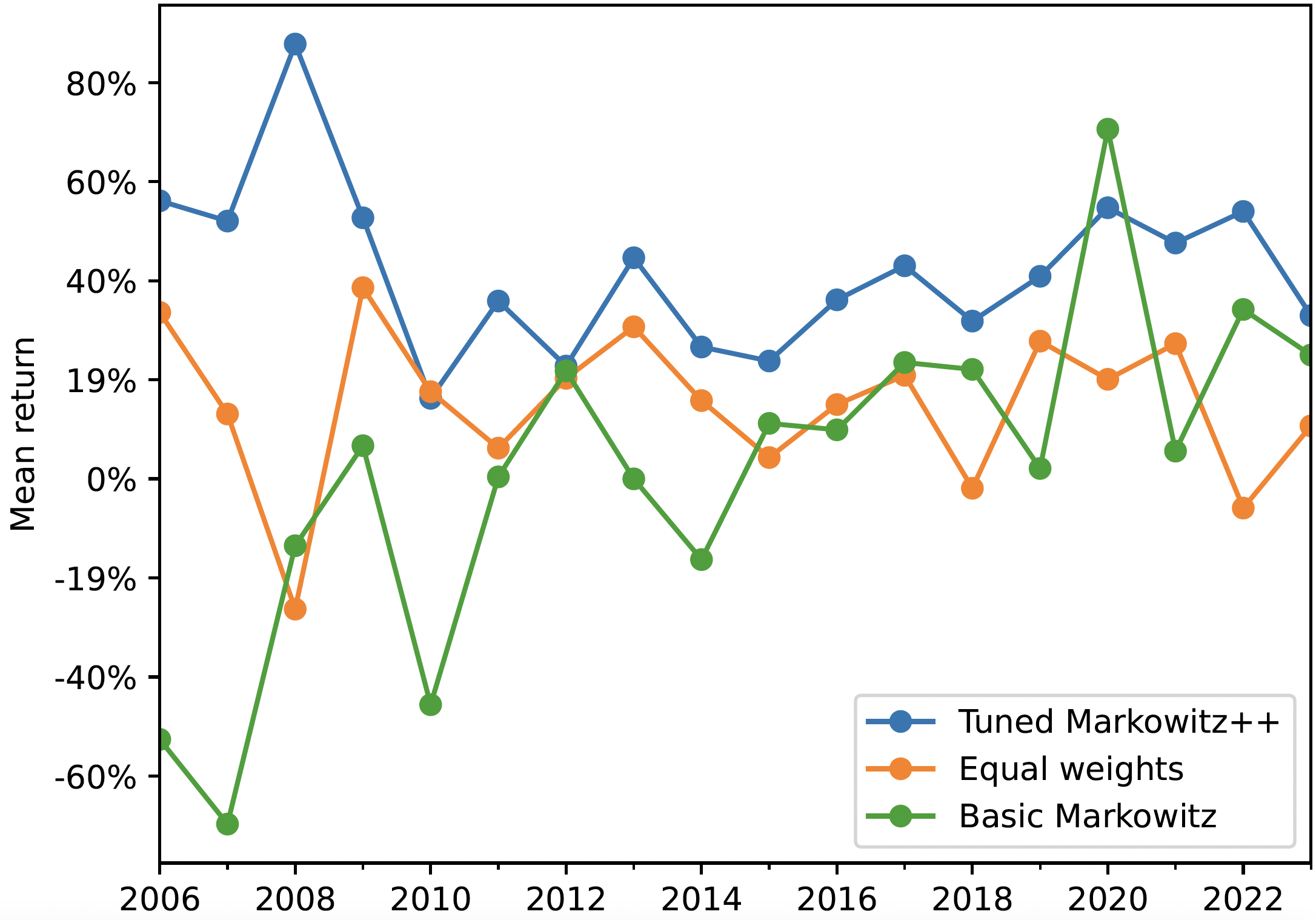

| Dec 24, 2023 | We published a preprint of our manuscript Markowitz Portfolio Construction at Seventy. A software package is available on GitHub. (Now published in The Journal of Portfolio Management, 2024.) |

| Dec 9, 2023 | We published a preprint of our manuscript Finding Moving-Band Statistical Arbitrages via Convex-Concave Optimization. (To appear, Optimization and Engineering, 2024.) |

| Sep 18, 2023 | I (successfully) completed my PhD qualifying exam. My slides are available here. |

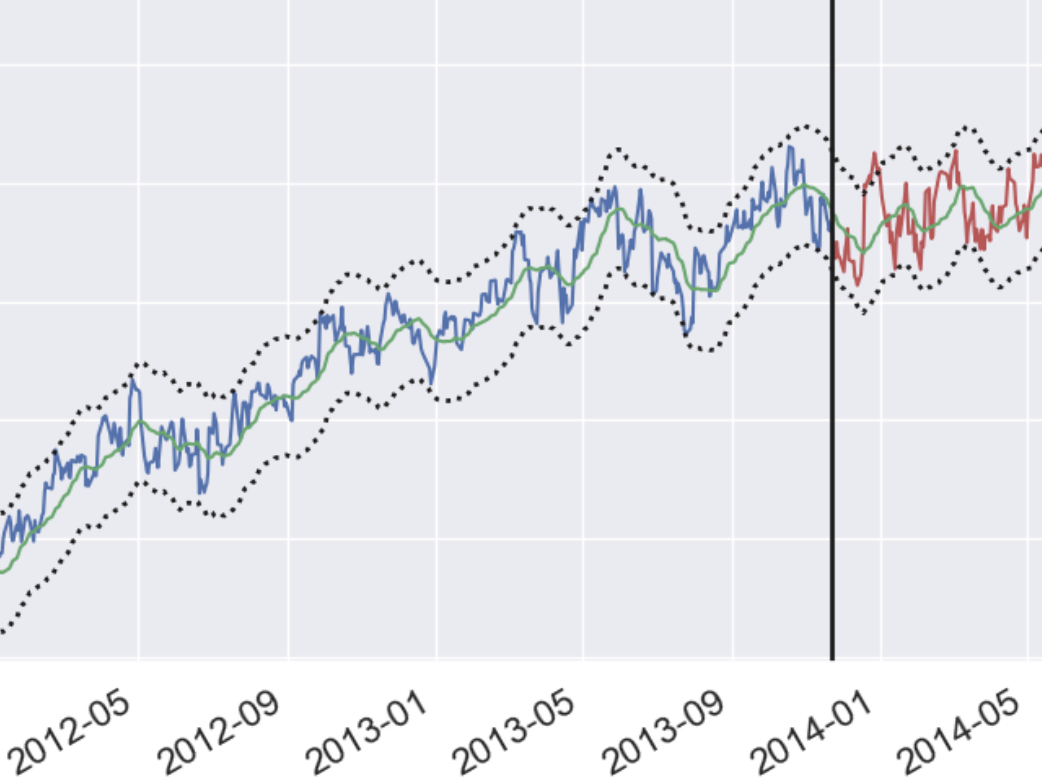

| Jul 11, 2023 | We published a preprint of our manuscript A Simple Method for Predicting Covariance Matrices of Financial Returns. (Now published in Foundations and Trends in Econometrics, 2023.) A software package is available on GitHub. |

selected publications

2025

-

Convex Optimization in Quantitative Finance2025PhD Dissertation Thesis, Stanford University

Convex Optimization in Quantitative Finance2025PhD Dissertation Thesis, Stanford University

2024

-

A Markowitz Approach to Managing a Dynamic Basket of Moving-Band Statistical Arbitrages2024Working Paper, Stanford University

A Markowitz Approach to Managing a Dynamic Basket of Moving-Band Statistical Arbitrages2024Working Paper, Stanford University -

Markowitz Portfolio Construction at SeventyJournal of Portfolio Management, Harry Markowitz Special Issue, 2024

Markowitz Portfolio Construction at SeventyJournal of Portfolio Management, Harry Markowitz Special Issue, 2024

2023

-

Finding Moving-Band Statistical Arbitrages via Convex-Concave Optimization2023Working Paper, Stanford University

Finding Moving-Band Statistical Arbitrages via Convex-Concave Optimization2023Working Paper, Stanford University -

A Simple Method for Predicting Covariance Matrices of Financial ReturnsFoundations and Trends® in Econometrics, 2023

A Simple Method for Predicting Covariance Matrices of Financial ReturnsFoundations and Trends® in Econometrics, 2023